CATEGORY - PAYMENTS

Payment Gateway Example With Use-Cases

Payments - 06 May, 2026

-

Table of Contents

Online payments are designed to feel simple. A customer selects a product, enters payment details, and completes a transaction in seconds. From the user’s perspective, the process appears instant and seamless.

Behind the scenes, each payment follows a structured flow involving multiple systems that handle data securely, verify funds, and move money between accounts.

This guide explains a payment gateway example end-to-end. It focuses on one complete transaction and uses it to explain how payment gateways work, who is involved, how integration is done, and what happens during testing and go-live.

Payment gateway defination for Merchants

A payment gateway is a service that securely collects, encrypts, and transmits payment information from a customer to financial institutions for authorisation, and then returns the result to the merchant in real time.

It acts as the interconnection between a business’s checkout system and the banking network. Without it, online payments cannot be processed securely or reliably.

Payment Gateway Example: A Complete Transaction Walkthrough

To understand how a payment gateway works, consider a simple example.

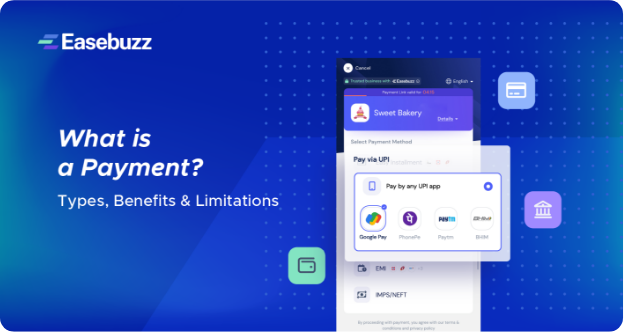

A customer visits an e-commerce website, adds a product to their cart, and proceeds to pay using a card or UPI.

This single action triggers a series of steps that happen within seconds.

-

1. Payment Initiation:

The customer enters payment details such as card information or UPI ID and clicks Pay Now. The website captures this information and prepares it for processing.

At this stage, the transaction has not yet been sent to the bank. It is still within the merchant’s checkout system.

-

2. Data Encryption and Tokenisation:

The payment gateway immediately encrypts the payment data using secure protocols such as SSL/TLS. In many cases, sensitive data is also tokenised, meaning the actual card details are replaced with a secure token.

This ensures that raw financial data is never exposed during transmission or storage.

-

3. Request Sent to The Acquiring Bank:

The encrypted request is forwarded to the merchant’s acquiring bank. This bank acts as the receiving institution for the merchant and is responsible for initiating the transaction into the payment network.

-

4. Network Routing:

The acquiring bank sends the transaction request through the appropriate network:

-

For card payments: Visa, Mastercard, or similar networks

For card payments: Visa, Mastercard, or similar networks

-

For UPI payments: the UPI infrastructure

-

-

5. Issuing Bank Authorisation:

The issuing bank (the customer’s bank) receives the request and performs several checks:

-

Validates card or account details

-

Confirms available balance or credit limit

-

Runs fraud detection algorithms

-

Verifies transaction authenticity

-

-

6. Response Returned to The Customer:

The decision is sent back through the same path:

Issuing bank → Network → Acquiring bank → Payment gateway → Merchant system

The website displays the result to the customer—typically within a few seconds.

-

7. Settlement of Funds:

Approval does not mean the merchant immediately receives the money.

Instead, approved transactions are batched and processed during settlement. The acquiring bank transfers funds to the merchant’s account based on a predefined cycle, usually T+1 or T+2 business days.

This separation between authorisation and settlement is a key concept in understanding payment gateways.

Who is Involved in This Payment Gateway Example?

Each transaction involves multiple participants working together:

-

Customer initiates the payment

-

Merchant provides the checkout and receives funds

-

Payment gateway encrypts and routes data

-

Payment processor facilitates communication between systems

-

Acquiring bank receives funds for the merchant

-

Issuing bank verifies and authorises the payment

-

Card network or UPI system routes the transaction

How Payment Gateway Integration Works

To enable this payment flow on a website or app, businesses must integrate a payment gateway into their system.

-

Selecting a payment gateway:

Businesses choose a gateway based on supported payment methods, fees, regional availability, and developer tools.

-

Merchant onboarding:

The business completes registration, submits required documents, and links a bank account. Once approved, the gateway provides API credentials.

-

API key configuration:

Payment gateways issue two sets of API keys:

-

Test keys for sandbox environments

-

Live keys for production

These keys authenticate communication between the merchant’s system and the gateway.

-

-

Building the integration:

Frontend

The frontend is responsible for collecting payment details securely. This can be done using:

-

Hosted checkout pages

-

Prebuilt SDKs

-

Custom forms with tokenisation

Backend

The backend handles transaction logic:

-

Creates payment requests

-

Sends requests to the gateway

-

Receives and stores responses

-

Updates order status

This separation ensures security and control.

-

-

Handling responses and edge cases:

A robust integration must handle different outcomes:

-

Successful payments

-

Failed or declined transactions

-

Pending or delayed responses

-

Duplicate requests

-

Testing a Payment Gateway

Testing is a critical step before accepting real payments.

Sandbox environment: Most payment gateways provide a sandbox environment where transactions can be simulated without real money.

What to test

A complete testing process includes:

-

Successful payments

-

Failed transactions

-

Incorrect details

-

Network timeouts

-

Refund and reversal flows

Why testing matters

Testing ensures that:

-

The integration works as expected

-

Errors are handled gracefully

-

The system remains stable under different conditions

Without proper testing, even small issues can lead to failed transactions or poor user experience.

Going Live With a Payment Gateway

After testing, the system can be moved to production.

-

Switch to live mode:

Replace test API keys with live keys to enable real transactions.

-

Complete verification:

Ensure that KYC, bank account linking, and compliance requirements are fully completed.

-

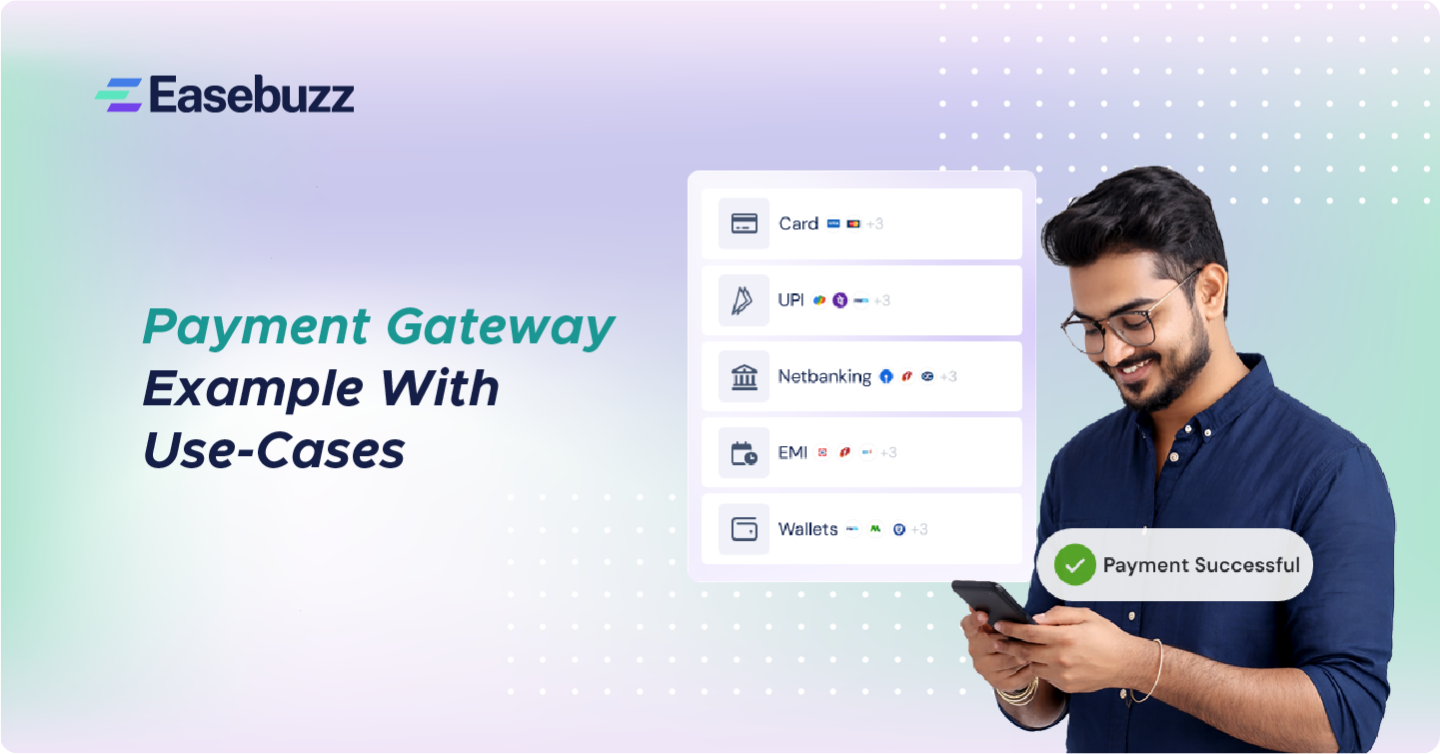

Enable payment methods:

Activate the required payment options such as cards, UPI, or wallets.

-

Monitor performance:

Track metrics such as:

-

Transaction success rate

-

Failure rate

-

Settlement timelines

Monitoring helps identify issues early and optimise performance.

-

Types of Payment Gateway Integrations

Different integration models are available depending on business needs.

-

Hosted payment gateway:

Customers are redirected to a secure page hosted by the gateway. This reduces development complexity and security responsibility.

-

API-based integration:

Payments are processed within the website or app, offering a seamless user experience and greater control.

-

Platform integrations:

Plugins are available for platforms such as Shopify or WooCommerce, allowing businesses to enable payments quickly.

Security in Payment Gateways

Security is a fundamental aspect of payment processing.

Key mechanisms include:

-

Encryption to protect data during transmission

-

Tokenisation to avoid storing sensitive information

-

PCI-DSS compliance to ensure industry standards

-

Fraud detection systems to prevent unauthorised transactions

These layers ensure that payment data remains secure throughout the process.

Common Misconceptions About Payment Gateways

Understanding what a payment gateway does also involves correcting common misunderstandings:

-

A payment gateway is not a bank

-

Payment approval does not mean instant settlement

-

Payment gateway and processor are not always the same

-

Faster checkout does not eliminate backend processing steps

Clarifying these points helps build a more accurate understanding.

Why Payment Gateways Matter for Businesses

Payment gateways are not just technical tools. They directly impact business outcomes:

-

Customer experience: smooth checkout reduces drop-offs

-

Revenue: higher success rates improve conversions

-

Scalability: support for multiple payment methods enables growth

-

Security: protects both customers and businesses

A well integrated gateway becomes a critical part of the overall product experience.

Conclusion

A payment gateway example is best understood as a complete system rather than a single step:

-

A customer initiates a payment

-

The gateway secures and transmits data

-

Banks and networks verify the transaction

-

The result is returned instantly

-

Funds are settled later into the merchant’s account

By following this structured flow, businesses can build reliable payment systems and users can better understand what happens behind every online transaction.

FAQ's

What is a payment gateway example in eCommerce?

In eCommerce, a payment gateway enables customers to pay via cards, UPI, or wallets at checkout. For example, when a user buys a product online, the gateway securely processes the payment, verifies it with banks, and confirms the order instantly. It also supports refunds, COD alternatives, and high transaction volumes, making it essential for smooth checkout and higher conversion rates.

How does a payment gateway work in quick commerce (10–15 min delivery apps)?

In quick commerce, speed and success rate are critical. A payment gateway ensures instant payment confirmation using UPI intent, saved cards, or one-click checkout. It must handle high concurrency, reduce failures, and support fast refunds. Real-time processing is essential because orders are fulfilled immediately after payment.

What role does a payment gateway play in retail businesses?

For retail, payment gateways unify online and offline payments. For example, a retailer can accept in-store payments via QR codes and online orders via website checkout. The gateway helps reconcile transactions, manage settlements, and provide a consistent payment experience across channels.

How is a payment gateway used in insurance payments?

In insurance, payment gateways handle premium collections, recurring payments, and policy renewals. For example, users can pay premiums via UPI autopay or cards. The gateway ensures secure transactions, supports mandates, and reduces payment failures, which is critical for policy continuity and customer retention.

How do payment gateways support education and edtech platforms?

Edtech platforms use payment gateways to collect course fees, subscriptions, and installment payments. For example, a student can pay via EMI, UPI, or cards. Gateways support recurring billing, flexible pricing, and global payments, making it easier to scale digital learning businesses.

What payment gateway requirements do Indian startups typically have?

Indian startups need gateways that support UPI, fast onboarding, and easy API integration. For example, a startup app integrates a gateway to accept payments quickly with minimal setup. They also require low transaction fees, high success rates, and developer-friendly tools to scale efficiently.

How do SMEs use payment gateways differently from large enterprises?

SMEs focus on ease of use and affordability. For example, a small business may use payment links, QR codes, or simple checkout plugins instead of full API integration. They need quick setup, minimal technical effort, and reliable settlements to manage cash flow effectively.

How do SaaS businesses use payment gateways for subscriptions?

SaaS businesses rely on payment gateways for recurring billing and subscription management. For example, a SaaS platform charges users monthly via cards or autopay. The gateway handles subscription cycles, failed payment retries, invoicing, and global payments, ensuring predictable revenue flow.

Share: