CATEGORY - PAYMENTS

Digital Wallets in India: What They Are, Types, Benefits & How to Use

Payments - 28 Mar, 2025

-

Table of Contents

The financial landscape is transforming rapidly, driven by the rise of digital payment solutions. As cash and traditional card-based methods wane, digital wallets have emerged as a secure, efficient, and convenient alternative for individuals and businesses.

In this article, we present a comprehensive guide to digital wallets. You’ll learn about their key features, explore various types, and understand the benefits they offer. Additionally, we discuss essential considerations to help you choose the digital wallet that best suits your financial needs.

What is a Digital Wallet?

A digital wallet is a secure software-based application that stores and manages your payment information, such as credit cards, debit cards, and bank account details. It enables seamless contactless payments, online transactions, and in-app purchases, reducing the need for physical cash or cards.

Functioning as a bridge between traditional banking and digital transactions, a digital wallet allows you to make payments effortlessly through smartphones, computers, or other connected devices. Many digital wallets offer enhanced security features, such as encryption, biometric authentication, and tokenisation, ensuring safe and convenient transactions.

Digital Wallet: Understanding Its Types, Features and Example

-

Closed Wallets

Features:

-

Specific to a single merchant or platform.

-

Funds can only be used within that platform.

-

Often, they offer loyalty programs and exclusive deals.

Examples: Amazon Pay Ballance, Flipkart Wallet, and Paytm Wallet.

-

-

Semi-Closed Wallets

Features:

-

Usable across affiliated merchants and service providers.

-

Broader usage than closed wallets.

-

It may require KYC (Know Your Customer) verification

Examples: Ola Money, PhonePe Wallet, and Swiggy Money.

-

-

Open Wallets

Features:

-

Offer the broadest range of functionalities.

-

Allow money transfers to other wallet users or bank accounts.

-

Often issued by banks or regulated institutions.

Examples: Google Pay, BHIM UPI.

-

-

Crypto Wallets

Features:

-

Designed to store, send, and receive cryptocurrencies.

-

Uses public and private keys for security.

-

Available as software (desktop, mobile, web) or hardware-based.

Examples: MetaMask, Trust Wallet.

-

-

Bank-Linked Wallets

Features:

-

Directly linked to bank accounts.

-

Enables seamless transactions using existing funds.

-

Integrated within mobile banking apps.

Examples: HDFC PayZapp, SBI YONO.

-

-

IoT Wallets

Features:

-

Integrated into smart devices like wearables.

-

Enable contactless payments on the go.

-

Ideal for small, frequent transactions.

Examples: Apple Watch Wallet, Fitbit Pay.

-

-

Mobile Wallets

Features:

-

Installed as smartphone apps.

-

Store multiple payment methods.

-

Utilize NFC or QR codes for transactions.

Examples: Google Wallet, Apple Wallet, and Samsung Wallet.

-

Advantages of Digital Wallets

-

Convenience & Speed: Swift payments with a tap or scan.

-

Enhanced Security: Encryption, biometric authentication, and tokenisation for fraud protection.

-

Cost Efficiency: Free or low-cost transactions.

-

Financial Management: Insights into spending habits.

-

Rewards & Cashback: Exclusive deals and discounts.

-

Contactless Payments: Safe and hygienic transactions.

-

Trackable Expenses: Simplified record-keeping.

-

International Money Transfers: Faster, often cheaper cross-border transactions.

-

Fraud Protection: Advanced monitoring systems.

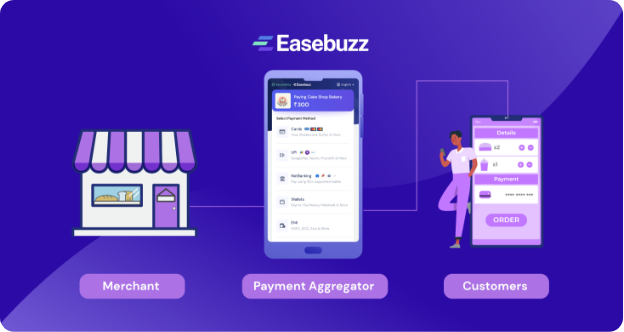

How Digital Wallets Work

Digital wallets streamline payments by securely storing financial details and enabling quick transactions. They consist of two key components:

-

Software Component: Connects to your bank accounts, encrypts data, and generates secure transaction codes.

-

Stored Information: Includes payment details, preferences, and transaction history.

When making a payment, the wallet communicates securely with payment gateways like Easebuzz, encrypting sensitive details and ensuring seamless transactions.

Technologies Used by Digital Wallets

-

NFC (Near-Field Communication): Enables contactless payments.

-

QR Codes: A cost-effective, secure method for transactions.

-

Tokenisation: Replaces sensitive data with unique tokens.

-

Biometric Authentication: Fingerprints, facial recognition for security.

-

Strong Encryption: Protects transaction data.

-

Real-Time Payments: Instant fund transfers.

-

Magnetic Secure Transmission (MST): Allows compatibility with older card-swipe terminals.

How to Use Digital Wallets: A Quick Guide

-

Download & Register: Choose a reputable digital wallet app.

-

Link Your Account: Connect bank account cards or add funds.

-

Make Payments: Tap, scan, or enter details at checkout.

-

Ensure Security: Use encryption, PINs, and biometrics for protection.

-

Track Transactions: Monitor spending with built-in tracking tools.

Digital Wallets in India: Benefits & Challenges

Benefits:

-

Contactless payments for hygiene and safety.

-

Faster transactions and reduced wait times.

-

Secure encrypted financial data.

-

Budgeting and tracking tools.

-

Cashback, rewards, and loyalty programs.

-

Financial inclusion for the unbanked population.

Challenges:

-

Security Risks: Potential vulnerability to hacking and data breaches.

-

Device Dependency: Requires a charged and functioning device.

-

Limited Acceptance: Not all merchants, especially in rural areas, accept digital wallets.

-

Internet Dependence: Transactions rely on stable connectivity.

-

Battery Drain: Continuous usage impacts device power.

-

Privacy Concerns: Collection of financial and personal data.

How to Choose the Best Digital Wallet

-

Security: Prioritize strong encryption and multi-factor authentication.

-

Compatibility: Ensure it works with your phone and preferred merchants.

-

User Feedback: Check reviews for reliability and performance.

-

Features: Look for bill payments, online shopping, and reward programs.

-

Ease of Use: Opt for a simple, intuitive interface.

Are there any fees/charges for digital wallets in India?

For Consumers:

-

Generally Free: Most digital wallets in India do not charge consumers for standard transactions like:

-

Peer-to-peer (P2P) transfers to other users or bank accounts.

-

Peer-to-merchant (P2M) payments at stores using UPI.

-

-

Wallet Loading:

-

Loading money into the wallet via UPI or bank transfer is usually free.

-

Some wallets may charge a fee (around 2-3% + GST) if you load money using a credit card. This varies between wallet providers (like Paytm, PhonePe, Mobikwik, Amazon Pay, etc.).

-

-

Withdrawal Charges: Some wallets might have charges for transferring funds from the wallet back to your bank account, but this is less common for general-purpose wallets.

-

Currency Conversion: If you use a digital wallet for international transactions, currency conversion fees will likely apply.

For Merchants:

UPI Payments:

-

For most bank-to-bank UPI transactions, merchants do not incur charges.

-

However, from April 2023, an interchange fee of up to 1.1% applies to merchants receiving payments above ₹2,000 through Prepaid Payment Instruments (PPIs) like digital wallets. This fee is paid by the merchant’s bank (acquirer) to the customer’s wallet issuer.

-

Payment Gateway Charges: If a merchant uses a specific payment gateway that integrates with digital wallets (like Easebuzz), they will have transaction fees as per the gateway’s pricing structure.

Key Points to Remember:

-

UPI is free for consumers for personal transactions. The new interchange fee primarily affects merchants for larger transactions via digital wallets.

-

Fees can vary between different digital wallet providers. It’s always a good idea to check the specific terms and conditions of the wallet you are using.

-

RBI Regulations: The Reserve Bank of India (RBI) regulates digital wallets and has issued guidelines on various aspects, including security and customer protection. While they don’t directly mandate fees for most consumer transactions, they oversee the framework within which these charges (like the PPI interchange fee for merchants) are applied.

Conclusion

Digital wallets have transformed how we handle transactions, offering convenience, security, and efficiency. With ongoing advancements, they will continue to integrate into our daily lives, reshaping commerce for the future.

FAQ's

Digital wallet in India

A digital wallet in India is an electronic way to store money and make payments using a smartphone or other digital device. It functions like a physical wallet but in a digital format, holding your payment information such as bank account details, credit/debit card information, and prepaid balances.

Popular Examples in India: Some of the widely used digital wallets in India include:

-

Paytm

-

PhonePe

-

Google Pay (GPay)

-

Amazon Pay

-

MobiKwik

-

Airtel Money

-

Ola Money

Are UPI and digital wallets the same?

No. UPI connects your bank account directly, while a digital wallet stores funds or card details.

How do digital wallets differ from UPI?

UPI offers direct online money/bank transfers, whereas a digital wallet holds stored money or saved card info.

Why should I use a digital wallet?

They are fast, secure, and convenient, with added rewards and offers.

Are digital wallets safe?

Yes, with encryption, tokenisation, and biometric security features.

Do digital wallets charge fees?

Most are free, but some may charge for premium features or international transfers.

Can I use a digital wallet without a bank account?

Yes, some wallets allow fund loading without direct bank linkage. Embrace digital wallets and experience a secure, cashless, efficient financial future!

Share: