CATEGORY - ECOMMERCE

Payment Options to Increase Conversion Rates: EMIs, BNPL, No-Cost EMI & Offers

ECOMMERCE - 3 Dec, 2025

-

Table of Contents

In today’s digital-first economy, businesses whether online or offline cannot rely on traditional payment modes alone. Customers expect fast, secure, and flexible ways to pay, and their purchase decisions often depend on whether a business offers these options at checkout.

From EMIs and BNPL to No-Cost EMI and smart offer engines, flexible payment methods are no longer add-ons—they are essential for improving conversions and reducing cart drop-offs.

At Easebuzz, we work closely with thousands of merchants across retail, education, travel, D2C commerce, SaaS, and more. We’ve seen firsthand how payment behaviour in India has changed over the last few years. The trend is clear:

Businesses that offer flexible payment options consistently achieve higher conversions, increased average order value (AOV), and better customer retention.

This article explains how EMIs, BNPL, No-Cost EMI, and smarter offer mechanisms work, why they matter, and how any business can implement them easily to boost conversions.

Why Flexible Payment Options Matter

Customer expectations have evolved rapidly, especially in the digital payments space. With rising smartphone penetration, UPI adoption, and credit alternatives, modern consumers prefer flexibility over high upfront costs.

Here are the key behavioural shifts driving this change:

-

Customers want affordability, not heavy upfront payments

Large-ticket purchases like electronics, tuition fees, fashion, appliances, and travel packages often get postponed if full payment is required. EMI and BNPL bridge this gap by breaking payments into smaller, manageable amounts. -

Checkout friction directly impacts conversions

Industry reports suggest that over 60% of cart abandonments in India happen due to payment concerns, lack of preferred payment mode, insufficient credit limit, or high upfront cost. When flexible payment options are offered, this barrier reduces significantly. -

Younger customers prefer instant credit alternatives

The 18–35 segment, which drives a majority of online purchases in India, is increasingly choosing BNPL over traditional credit cards due to its instant approval and simplicity. -

Flexible payment options increase trust in digital transactions

When a business offers multiple payment options including EMIs it signals reliability, security, and transparency. This directly increases customer confidence.

What Are EMIs, BNPL & No-Cost EMI?

Let’s break down the most popular flexible payment options and how they work.

Card EMIs

Card EMIs allow customers to convert their purchase amount into monthly instalments using their credit or debit cards.

-

Best for: Electronics, appliances, furniture, education fees, healthcare, travel, large ticket D2C items.

-

Value for customers: Pay in smaller chunks instead of one large amount.

-

Value for businesses: Increases sales of premium products and reduces drop-offs.

No-Cost EMI

In No-Cost EMI, customers pay the exact product price over installments without any interest.

-

Best for: High-demand, price-sensitive categories electronics, mobiles, fashion, consumer durables.

-

Why it converts more: Customers perceive high value since the overall cost doesn’t increase.

BNPL (Buy Now, Pay Later)

BNPL gives customers instant credit at checkout with minimal documentation. They can pay the full amount later or split it into installments.

-

Best for: D2C brands, fashion, beauty, food, travel, utilities, subscription services.

-

Why it works: Easy approval, low friction, preferred by young shoppers.

Offer Engine (Cashbacks, Discounts & Dynamic Offers)

An offer engine allows businesses to run category-specific, bank-specific, seasonal, or personalised offers.

Examples

-

Cashback on UPI

-

Additional 10% discount on specific card networks

-

Instant discount during festivals

-

Exclusive partner offers

Why it helps: Real-time offers create urgency, improve customer experience, and boost impulse purchases.

How Flexible Payment Options Improve Conversion Rates

Businesses integrating EMIs, BNPL, and offers experience a noticeable improvement in their overall sales metrics. Here’s how:

-

They reduce checkout drop-offs

-

Customers often abandon carts due to the burden of upfront payment or inability to pay full amount immediately.

-

Flexible payments remove this friction.

Example: A ₹25,000 mobile phone becomes much more affordable at ₹1,250/month.

-

-

They increase average order value (AOV)

-

When payments can be split, customers generally purchase higher-value products or add more items to their cart.

Result: AOV increases by 20–40% in categories where EMI/BNPL is available.

-

-

They build trust & credibility

-

Offering multiple payment methods signals that the business is secure, established, and customer-first.

-

-

They improve repeat purchases

-

When customers have a smooth payment experience, especially via BNPL or EMIs, they return for future purchases.

-

-

They enhance customer satisfaction

-

Affordability + flexibility = better experience = more conversions.

-

Best Payment Options for Businesses

Let’s explore each payment method with benefits and use cases for businesses.

-

Card EMIs

-

Allow customers to break high-value payments into manageable instalments

-

Accepted widely by Indian banks

-

Increase conversions for big-ticket categories

-

Electronics stores

-

Furniture retailers

-

EdTech platforms

-

Healthcare services

-

Travel agencies

-

Online marketplaces

-

Higher sales during festive seasons

-

Greater conversions without heavy discounting

-

Liquidity remains intact merchant gets full payment upfront

-

No-Cost EMI

-

No interest charged → higher customer confidence

-

Works well in competitive markets where price comparison matters

-

Encourages purchase of premium and mid-range items

-

Smartphones

-

Wearables

-

Home appliances

-

Lifestyle and fashion items

-

Attracts price-sensitive customers

-

Drives impulse purchases during sales

-

Helps brands compete without reducing base price

-

BNPL (Buy Now, Pay Later)

-

Minimal documentation

-

Instant approval

-

Perfect for younger shoppers

-

Available across categories, including low-ticket ones

-

D2C brands

-

Fashion and apparel

-

Cosmetics

-

Food delivery

-

Train/flight tickets

-

Travel packages

-

Lower bounce rate

-

More conversions for mid-ticket purchases

-

Improves customer loyalty with repeat usage

-

Offer Engines

-

Boost sales during festivals and campaigns

-

Personalise offers based on user behaviour

-

Reduce the need for heavy discounting

-

Engage customers with real-time benefits

-

Flat discount

-

Cashback on UPI/cards

-

Bank-specific offers

-

Combo offers

-

Wallet-based offers

-

Higher engagement

-

Competitive advantage

-

Strategic pricing flexibility

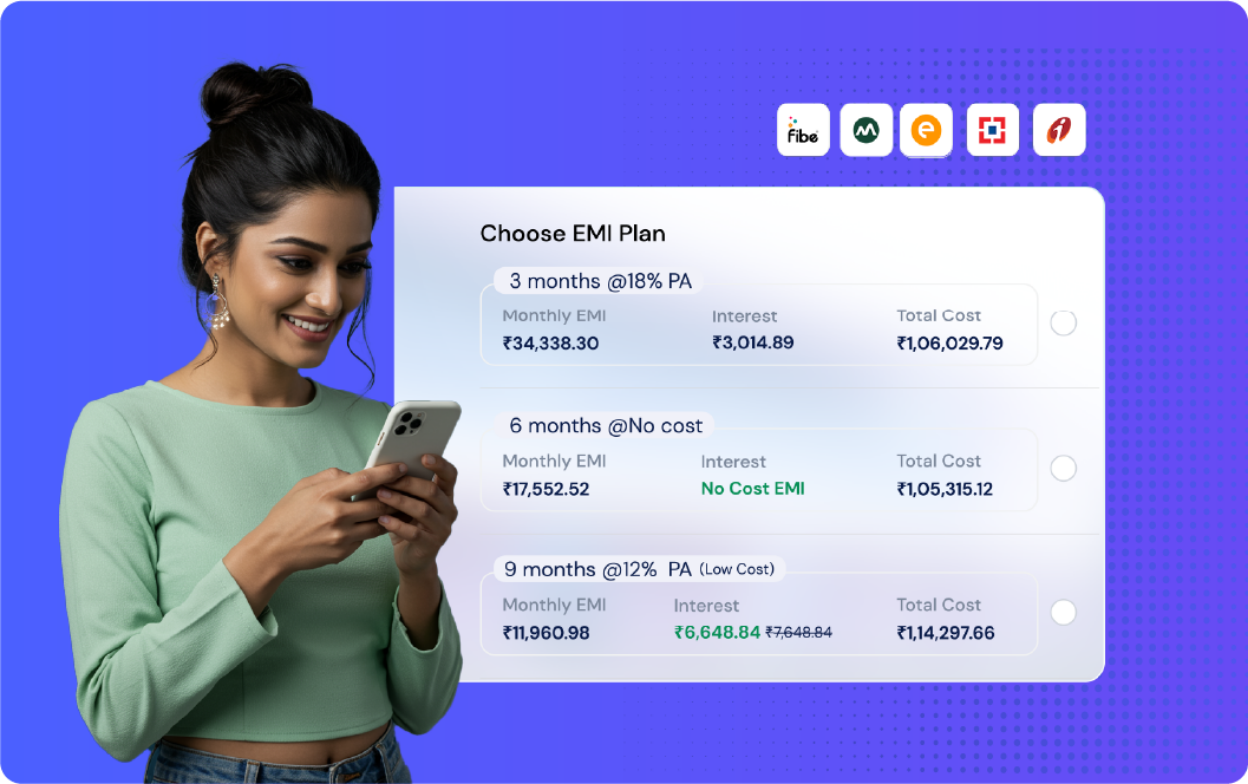

Why Card EMIs Matter

Industries That Benefit Most

Business Advantages

Why No-Cost EMI Converts Better

Best For:

Business Benefits:

Why BNPL is Growing Fast in India

Best For:

Business Benefits:

Why Offer Engines Are Critical for Conversions

Types of Offers You Can Run:

Business Benefits:

How Online & Offline Businesses Can Use These Options

Whether you sell online or offline, flexible payments work equally well.

For Online Businesses:

- Display EMIs and BNPL directly on the product page - Helps customers make a decision early.

- Enable EMI/BNPL at checkout - Reduces last-step drop-offs.

- Offer No-Cost EMI during festivals/sales - Boosts campaign conversion.

- Use an offer engine for dynamic promotions - Provide discounts based on card type, time period, order value, etc.

- Add EMI options on payment links and invoices - Useful for EdTech, healthcare, and service-based businesses.

For Offline Businesses:

- Provide EMIs at POS terminals - Customers can convert payments on the spot.

- Use QR-based BNPL or UPI credit - Enable instant credit through QR scans.

- Showcase “EMI Available” signboards - Helps drive walk-in conversions.

- Offer seasonal discounts with bank partners - Boosts footfall and in-store sales.

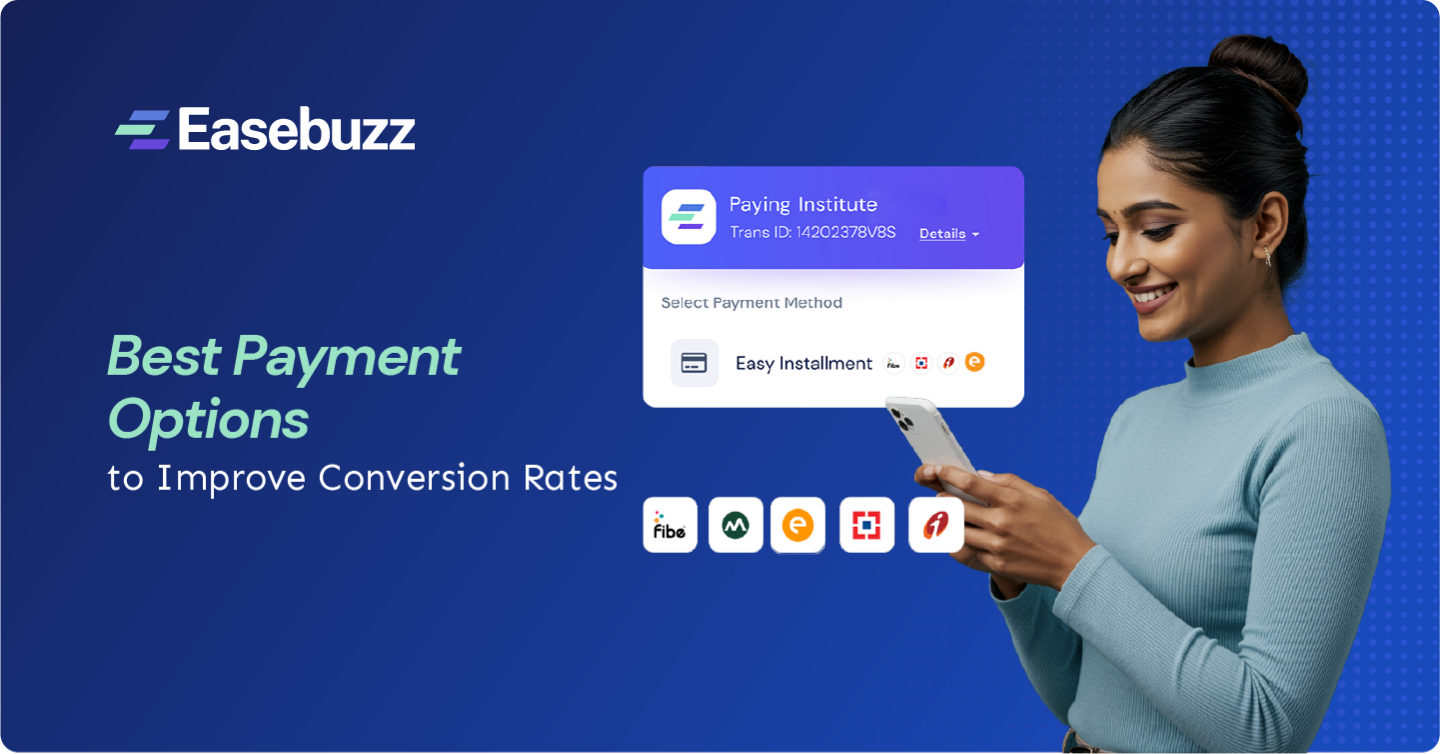

Why Easebuzz is the Best Platform to Enable These Payment Options

Easebuzz enables businesses small, medium, and enterprise to offer EMIs, BNPL, No-Cost EMI, and customised offers with minimal effort. Our platform is designed for scalability, performance, and flexibility.

Key Capabilities from Easebuzz:

- 150+ Payment Modes (UPI, cards, net banking, BNPL, wallets, EMIs, and more.)

- EMI Support Across Debit & Credit Cards

- Trusted by leading banks and card networks.

- BNPL Integrations with Top Lenders

- Instant approvals, One-click checkout.

- No-Code & API Integration Options

- Easy onboarding for businesses of all sizes.

- Smart Offer Engine

- Run dynamic offers and real-time discounts to boost conversions.

- Real-time Dashboard & Analytics

- Track payments, settlement, customer behaviour, and performance insights.

- Industry-Grade Security & Compliance

- PCI-DSS compliant, secure, and built for scale.

- Instant Settlements & 99%+ Success Rates

- Ensures a smooth checkout experience for your customers.

How These Options Directly Impact Business Growth

Flexible payment options don’t just improve conversions; they create a long-term impact on business growth.

- 25–40% higher conversion rates: Customers convert faster when they see affordable payment choices.

- Better customer experience: A frictionless, modern checkout boosts brand perception.

- Higher average order value: Customers confidently purchase premium products.

- Reduced cart abandonment: Flexible payments solve the #1 barrier upfront cost.

- Improved customer loyalty: BNPL and EMI users often return for repeat purchases.

Conclusion

The modern customer expects flexibility, speed, and convenience at checkout. Businesses offering EMIs, BNPL, No-Cost EMI, and smart offers already have an edge higher conversions, improved AOV, and stronger customer loyalty.

For businesses aiming to scale during peak time, flexible payment becomes more essential.

Easebuzz helps businesses of all sizes seamlessly enable these options through powerful APIs, no-code tools, EMI/BNPL integrations, and a smart offer engine designed to maximise conversions.

Whether you’re an online store, offline retailer, D2C brand, education platform, travel business, or subscription-based service, flexible payment solutions will play a critical role in your growth. And at Easebuzz, we’re committed to helping you unlock that growth securely, affordably, and at scale.

FAQ's

How do EMIs and BNPL help businesses increase conversions?

EMIs and BNPL reduce the customer’s upfront payment burden, making products more affordable. This leads to fewer cart drop-offs, higher average order value (AOV), and an increase in completed transactions, especially for mid-to-high-ticket items.

What types of businesses benefit the most from offering EMIs or BNPL?

EdTech, electronics, D2C brands, healthcare, travel, furniture, retail stores, and subscription-based services see the strongest impact. Any business selling products or services above ₹2,000 can benefit from flexible payments.

Is No-Cost EMI better than BNPL for boosting online sales?

No-Cost EMI works best for high-value purchases where customers compare pricing. BNPL is better for fast-moving categories like fashion, beauty, travel, and D2C where instant approval and quick checkout matter more. Both improve conversions but serve different customer segments.

Does offering EMIs or BNPL affect the business’s cash flow?

No. With payment aggregators like Easebuzz, the merchant receives full settlement upfront. The customer repays in installments to the bank or BNPL provider, not the merchant.

Are EMIs and BNPL difficult to integrate on a website or app?

Not at all. Platforms like Easebuzz offer no-code options, plugins, checkout integration, and APIs that make it easy for any business, small or enterprise to enable EMIs, BNPL, and offers within minutes.

Do flexible payment options increase operational costs for businesses?

Some payment methods may have associated MDR or interest subvention (for No-Cost EMI). However, the increase in conversions, order value, and repeat customers usually outweighs the added cost. Most businesses treat it as a customer acquisition investment.

Can offline businesses also offer EMIs and BNPL?

Yes. Offline merchants can offer card EMIs via POS machines, UPI-based BNPL, QR codes, or payment links. Many retailers use in-store offers and banners to promote flexible payment availability and boost walk-in conversions.

How does Easebuzz support businesses in enabling EMIs, BNPL, and flexible payment options?

Easebuzz provides:

-

150+ payment methods

-

Debit/Credit card EMI support

-

BNPL integrations with trusted lenders

-

No-code and API options

-

Intelligent Offer Engine

-

Real-time analytics & settlements.

This helps businesses instantly enable flexible payments without technical complexity.

Share: